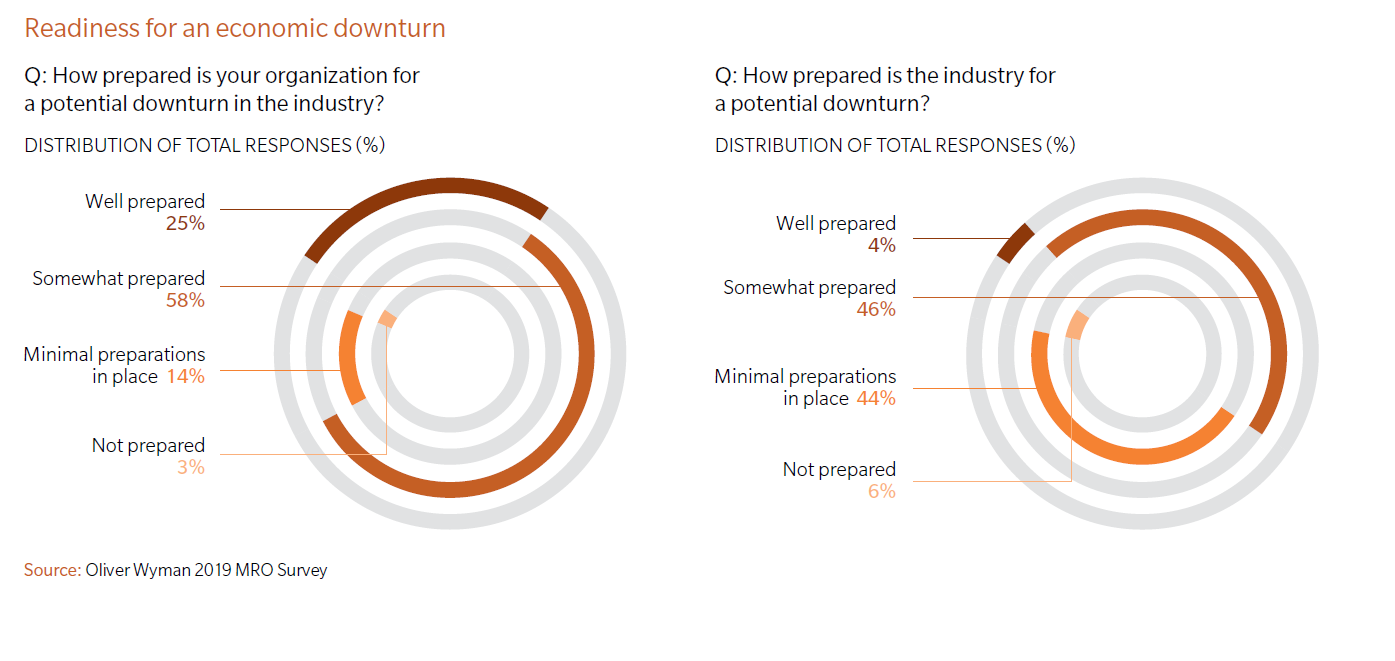

A decade of uninterrupted industry growth and some developing global headwinds raise concerns about whether an economic contraction is on the horizon. Our Global Fleet & MRO Forecast for 2019-2029, however, projects a strong ten years ahead with minimal downside due to the longtail regulatory required maintenance protocols for aircraft. Meanwhile surveyed market participants are also optimistic despite rising geopolitical and possible trade upheavals, rising interest rates, and fluctuating fuel prices. Even if the global economy slows, three-quarters of survey respondents believe their organizations are ready to ride out rough weather, yet were less bullish on the preparations across the broader aviation industry. This disconnect may suggest that there is an opportunity for more formal planning and preparation for the inevitable downturn in a traditionally cyclical industry.

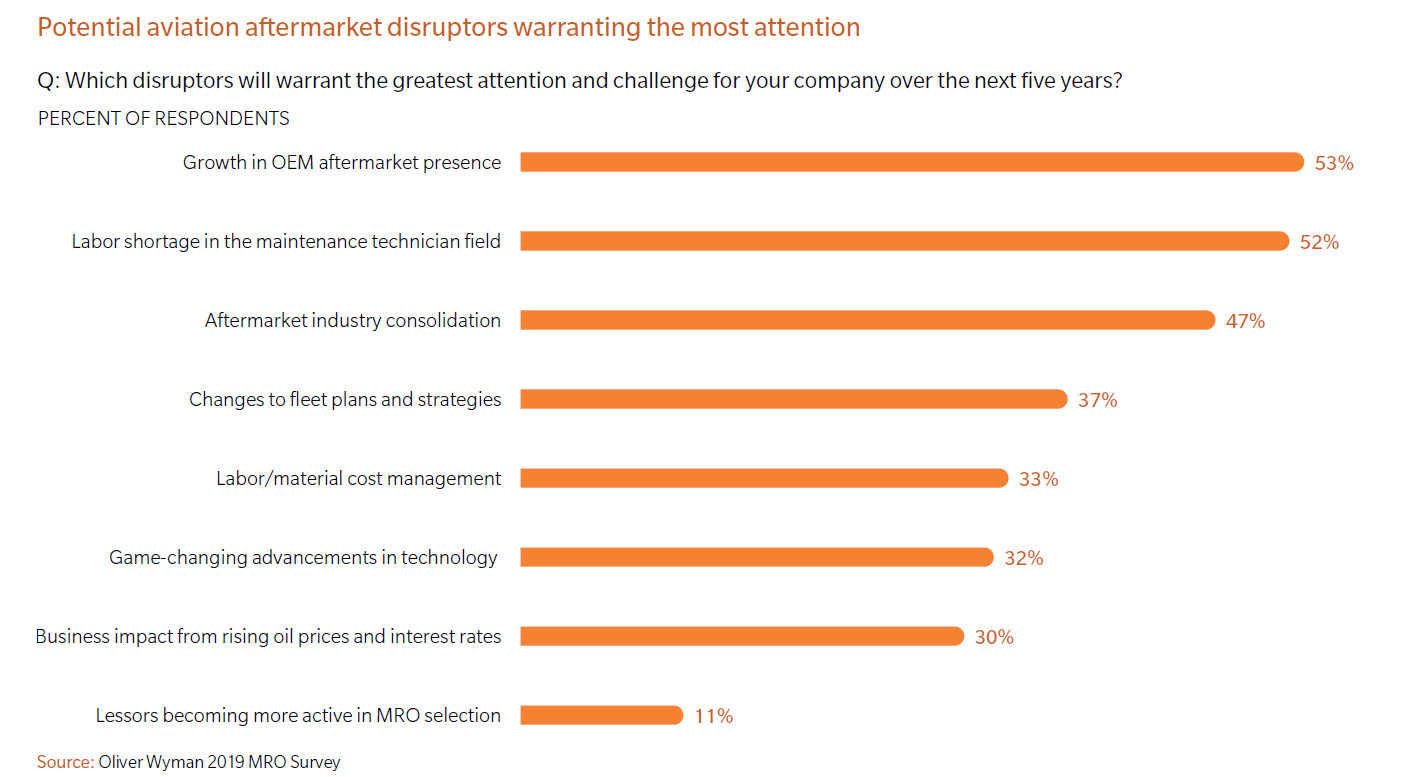

We also ask industry participants every year about potential top market disruptors, and once again OEM expansion topped the list, with airframe OEMs expected to utilize all available channels to push further into the MRO market. At the same time, airlines are concerned that they have balanced and competitive options for MRO, which may lead them to develop new suppliers or redevelop some of their own technical capabilities to counter the OEM surge. Some signs of airlines further investing in their captive MRO services or bringing work back in house are popping up.

We believe that there is room and a need for standalone MRO providers that are well tooled, efficient, and cost effective. But as OEMs increase their aftermarket penetration, these MROs will be challenged to develop more customized service approaches and capabilitiesBrian Prentice, Aviation Partner and Lead Author

Finally, digital services continue to evolve but have not yet become essential to winning work in the marketplace. While seeing value in innovations such as aircraft health management and predictive maintenance, airlines remain unsure who should provide these services or how best to benefit from them. For now, when it comes to choosing an MRO provider, the classic trifecta of cost, timeliness, and high-quality service still matters most.

Oliver Wyman Partner David Stewart presents the Industry Trends and Forecast.

About the survey

In its second decade, the Oliver Wyman annual MRO survey is an industry standard that samples the attitudes and strategies of executives from across aviation as they address key trends and emerging issues in the maintenance, repair, and overhaul (MRO) sector. Some 130 global aviation professionals responded to the 2019 survey, drawn from a cross-section of airline operators, captive airline MROs, independent MROs, and original equipment manufacturers (OEMs). Representatives from leasing organizations, financiers, parts distributors, and advisors rounded out the ecosystem of respondents.

This year, 46 percent of respondents to the annual survey were senior executives – either in C-suite posts, vice presidents, or above; nearly 80 percent were director level or above. And this year’s survey was our most global yet, with more than half of respondents’ companies headquartered outside of North America and three-quarters reporting primary bases of operations outside of North America and Western Europe.

Oliver Wyman Ideas App